Meet RMP, the New Name for Endless QE

- May 19

- 4 min read

"I think shrinking the [Fed] balance sheet is the wrong objective." - Fed governor Barr.

With inflation through the roof, inflation expectations sky high, and the economy excluding AI in a recession, the Fed is printing money.

But it's not QE anymore - the new name is RMP.

Last week, Fed governor Michael Barr gave a speech defending Fed money printing.

Inflation, as measured by CPI, is already higher than the Fed funds rate. The Fed is cutting rates. But that's not enough.

As per Barr, the Fed needs to expand its balance sheet as well.

Barr starts by simplifying the Fed balance sheet. On the assets side, we have US treasuries and mortgage-backed securities accumulated from 18 years of QE.

The liabilities consist of cash in circulation, bank reserves at the Fed, and deposits at the Treasury General Account.

Ex-chair Powell, for all his faults, did try to shrink the asset base at least a little bit.

Barr says that's the wrong approach.

From Barr's speech:

"In keeping with our commitment to effective implementation, after substantially shrinking the balance sheet for a couple of years, the Fed is now slowly growing our balance sheet to keep up with demand for our liabilities."

Barr's argument is that the Fed needs to buy assets because there's growing demand for its liabilities.

Not because it is good policy or the right thing to do. Barr says the Fed should give the market what it wants.

If he has his way, it will be apparent to the whole world that the Federal Reserve is a private institution captured by the commercial banking system.

The veneer of central bank independence will have served its purpose.

Putting aside the ethics of it, is there any merit to Barr's argument?

Should the Fed buy more Treasuries (a balance sheet asset) to 'keep up' with rising demand for reserve balances (a BS liability)?

To answer this, one has to understand why banks hold reserves at the Fed.

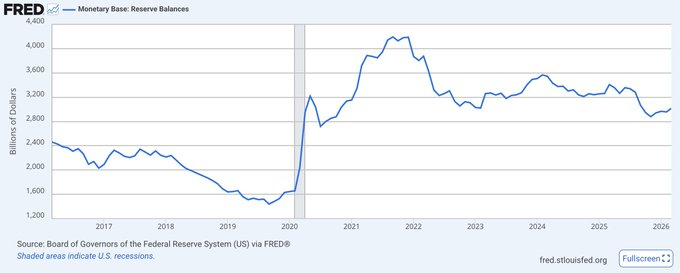

Every time a commercial bank expands its balance sheet through deposits and loans, a portion of it gets parked at the Fed.

The Fed controlled the reserve ratios, increasing reserve requirements during bull markets to rein in excess lending, and lowering them during recessions to encourage credit expansion.

This was thought to be the proper function of a central bank in an industrialized society.

Until 2008, commercial banks held only the statutory minimum in reserves with the Fed. The Fed did not pay any interest on these reserves, and lending was profitable, so banks lent.

This was the era when a retiree could build a CD ladder and retire on interest income.

Then came Quantitative Easing, the fancy term for money printing.

The Fed bought the assets parked in bank balance sheets using freshly printed money.

The banks, scarred from the credit collapse, stopped lending and instead began parking excess reserves with the Fed.

The Fed paid interest on these excess reserves.

It was free money for banks, with zero credit risk since their counterparty was their regulator.

As a result of this policy, bank lending failed to recover even after QE 1, QE 2, QE forever and Operation Twist (this was the gap filled by private credit, but that's a story for another day).

Then came Covid, another excuse to print money.

The Fed also made another switch - banks would now get free money on ALL reserves.

Next came the big, fat bonus for doing absolutely nothing.

Ex-chair Jerome Powell announced rate hikes, handing out more free money for nothing.

A few silly bankers, mostly regional institutions, had lent out money into the real economy instead of sucking at the Fed's teat.

The rate hikes killed their client base, forcing them into receivership or the hands of more connected institutions.

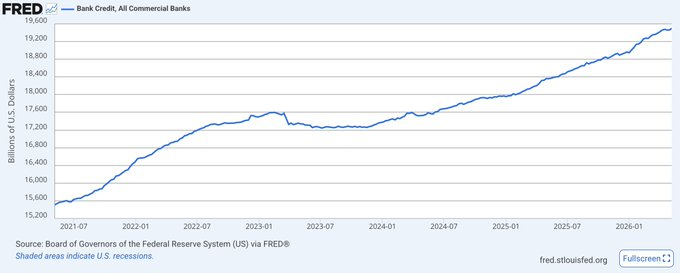

The big banks got even bigger, the regional bank crisis passed, and loan growth took off.

Bank deposits grew alongside, creating a need to maintain higher reserve balances at the Fed.

The proper function of a central bank, if you believe they should be allowed to exist, is to rein in credit during the boom, and supply liquidity during the bust phase of the business cycle.

Barr's argument turns central bank theory on its head.

Banks are parking more reserves at the Fed because they are lending more.

Since reserves are a Fed liability, and they are getting added, he says the Fed needs to balance it out by adding more assets.

In effect, Barr is arguing that the Fed needs to expand its balance sheet because the commercial banks are expanding theirs!

All credit growth is inflationary. If the Fed grows its balance sheet right alongside the banks, the end result will be banks increasing lending at a faster clip, forcing the Fed to expand its own balance sheet faster to 'catch up', resulting in massive inflation.

This is how we get to Project Zimbabwe.

In conclusion, the Fed's reserve management program, or QE by another name, is flawed at its very root.

Excessive reserve growth is a symptom of excessive bank lending activity and the central bank needs to rein it in, not add gasoline to the fire.

One last point. Barr says creating reserves is costless to the Fed. It most definitely is not!

The Fed is losing money by paying interest on these reserves. Instead of booking the losses and reducing its equity, it is hiding it under this balance sheet item - Earnings Remittances Due to the U.S. Treasury.

The Fed is currently sitting on $240.6 billion in realized losses. If Barr has his way and banks are encouraged to lend and park reserves with the Fed, this 'deficit' will soon start to rival that of the US Treasury.

The world's largest government and largest central bank are both broke.

The bond vigilantes have noticed this with respect to US Treasuries.

The dollar vigilantes will soon figure this out as well.

And that will be the end of US dollar hegemony.

Like what you read? Get more exclusive content by subscribing to my premium newsletter!

Good Trading!

Kashyap

Comments